Life Cycle Costing Updates

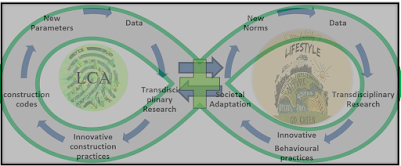

Most of India's habitat and civil infrastructure is yet to be built. The existing ones need rehabilitation and to be built better. The "LiFE mission" without enabling and integrating the construction industry is incomplete.

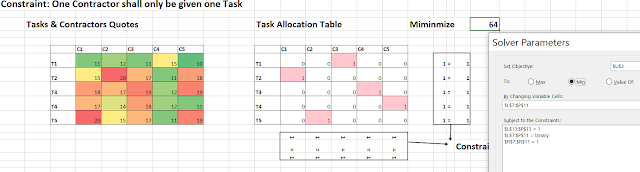

Decision Making Through Life Cycle Costing- A Simple Practical Example

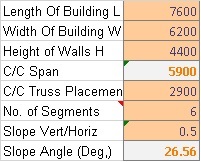

Life Cycle Costing-2: A Practical Project Feasibility Example

Supporting Green Decisions With Financial Simulations

Using Excel's Forecast Sheet Feature for Construction & Life Cycle Parameters

The LCC of a Project needs to evolve and follow frameworks and a baseline. ISO: 14040 provides a broad framework that ensures that LCC is conducted rigorously and transparently.

ISO: 15686-5: 2017 guides the practitioners in defining the goal and scope, fixing system boundaries, reference study period, discount rates and sensitivity analysis parameters. The relevant costs and calculation methods are done in the Life Cycle Inventory phase. Analysing costs, comparing results, and drawing conclusions is the interpretation phase of the Life Cycle. The concluding, reporting, and critical reviews of LCC analysis are perhaps the most important aspect of the whole exercise. The method details, assumptions, limitations, and implications of LCC must be followed up for validation. All phases of LCC require expert judgements which would get refined with every new project.

Besides Mission LiFE, Sendai Framework on Disaster Risk Reduction and Sustainable Development Goals (SDGs) framework is shaping and evolving new professional challenges on resilient and cost-effective infrastructure. One size won't fit all projects, and adopting Life Cycle Costing would be more challenging than ever.

The National Building Code of India does not explicitly cover provisions on the Life Cycle Costing or assessment, but this should not deter the Construction teams from going for the Life Cycle costing of Projects. As defined in part Zero of NBC, collaborative teams must gear up to resolve all Life Cycle Costing issues and create and integrate value delivery.

An ounce of practice is better than tonnes of theory. In her PhD dissertation, Dr Priyanka Kochhar evaluated three CPWD Institutional Buildings, which provide us with many practical aspects of the above theory. I wish the analysis part had been done in Excel, enabling the practitioners to create their own scenarios. Even then, there is no valid reason why all government construction procurements should not follow the Life Cycle methodologies in decision-making.

Life Cycle Costing (LCC) is a financial analysis method that assesses the total cost of ownership of a project or asset over its entire lifespan. This approach considers all costs associated with the acquisition, operation, maintenance, and disposal of an asset, helping organizations make more informed financial decisions. Here’s an overview of key components and benefits:

ReplyDeleteKey Components of Life Cycle Costing:

Acquisition Costs:

Initial purchase price or construction costs, including any associated fees (e.g., permits, taxes).

Operating Costs:

Ongoing expenses for operating the asset, such as utilities, labor, and materials.

Maintenance Costs:

Expenses related to regular maintenance, repairs, and upgrades needed to keep the asset functioning effectively.

Financing Costs:

Interest and fees associated with financing the purchase or construction of the asset.

Depreciation:

The reduction in value of the asset over time, which can impact financial reporting and tax obligations.

End-of-Life Costs:

Costs associated with the disposal, decommissioning, or recycling of the asset at the end of its useful life.

Benefits of Life Cycle Costing:

Informed Decision-Making:

Provides a comprehensive view of costs, enabling better budgeting and financial planning.

Cost Optimization:

Identifies opportunities to reduce total costs through efficient design, procurement, and maintenance practices.

Long-Term Perspective:

Encourages organizations to consider long-term implications rather than focusing solely on initial costs.

Sustainability Considerations:

Promotes sustainable practices by factoring in environmental and social costs, such as energy consumption and waste management.

Risk Management:

Helps in identifying potential risks and uncertainties related to costs over the asset's lifecycle.

Applications of Life Cycle Costing:

Construction Projects: Used to evaluate the total cost of buildings and infrastructure over their operational lives.

Manufacturing: Applied to assess costs associated with machinery and equipment from acquisition through operation to disposal.

Public Sector: Utilized in government projects to justify investments based on long-term financial benefits.

Big Data Projects For Final Year Students

Image Processing Projects For Final Year

Deep Learning Projects for Final Year

Articles on Monaco Report combine global and local perspectives, offering readers expert insights on economic, technological, and lifestyle developments that shape Monaco’s present and future.

ReplyDeleteArticles on Laos Wire combine global perspectives with local relevance, offering readers valuable insights on technology, social media, entertainment, and finance to understand trends shaping everyday life.

ReplyDeleteCovering travel adventures, cultural exploration, and lifestyle experiences, PopDengClick provides readers with insightful articles that encourage curiosity, learning, and enjoyment of the world around them.

ReplyDelete